A message from the

President and Chief Executive Officer

“Our culture is what delivers a great experience for our clients who in turn reward us with their trust and ultimately their business. This is our formula for success.” Douglas L. KennedyPresident and Chief Executive Officer

On behalf of the talented and hard-working employees of Peapack-Gladstone Bank, I am happy to report yet another year of record performance for our company. We reported net income of $44.2 million—$45.3 million on a core basis, resulting in a 24% increase year-over-year. And, we reported fully diluted earnings per share of $2.31—$2.37 on a core basis, resulting in a 17% increase compared to 2017. Notwithstanding this solid gain in profitability, our share price declined 28% to close at $25.18 at year end. Our stock has recovered somewhat in early 2019, and we firmly believe that with patience and discipline, we will deliver superior shareholder value over time.

Our company ended the year with total core revenues of $161 million, loan outstandings of $3.9 billion, deposits totaling $3.9 billion, and total capital of $469 million. Every one of these measures was a record level of achievement. Commercial and Industrial (C&I) loans, including equipment finance, grew by 46% or $440 million to $1.4 billion, deposits grew by $197 million or 5%, wealth management fees grew by $10.1 million or 43%, and our net income has grown at a compounded annual rate of 30% since the launch of our strategy, Expanding Our Reach, in 2012.

Much of our growth in profitability has been the result of the “scale” we have built in both our commercial banking business and in our wealth management division. We believe these core businesses, that will serve as the foundation of our future growth, present great opportunity as a niche player in the New York metropolitan market. Both businesses are built on providing sound, unbiased advice that leverages people and relationships, supported by technology, and our team consistently delivers a differentiated level of service. At Peapack-Gladstone Bank, we empower our employees to act in the best interest of our clients with no proprietary products and no bias. This approach has enabled us to attract a significant number of high performing professionals from large institutions where employees feel less valued. Our focus on the metropolitan New York market provides us with great talent and ample opportunity to deliver attractive shareholder returns.

Market Conditions Tightened in 2018

Net interest margin compression, the difference between what we pay for deposits and what we charge for loans, really began to tighten in 2018. The Federal Reserve increased short-term rates by 1% during the year and many depositors, who had been receiving virtually no interest on their deposits over the last several years, began to focus more on receiving higher returns. Rates increased dramatically over the year and we, as did all banks, needed to respond. In addition to dealing with higher short-term rates, the reversal of Quantitative Easing (QE) stimulus programs implemented during the financial crisis began the process of shrinking the money supply. Over the next few years, the U.S. Treasury expects to reduce the money supply by $1.5 trillion. Both actions by the government will impact interest rates over time and challenge us to carefully manage our balance sheet, capital, and operating costs. Deposits are an essential element to generating loans, and we remain focused on attracting deposits.

On the wealth management front, the stock market experienced its worst December performance in nearly 50 years. While we have seen some recovery in early 2019, higher levels of volatility are anticipated this year as we believe we are moving closer to the completion of what has become the longest economic expansion in history.

All of these market conditions cause us to be more cautious and disciplined as we focus on the next few years

Core Fee Income Grew 32% in 2018 to 28% of Total Revenue

We grew fee income across the board in 2018, with wealth management fee income experiencing the largest gain. Wealth management fees were up $10.1 million or 43% year-over-year and now contribute 21% of total revenue for our company. Our two to three-year plan is to grow total fee income to 35%–45% of our total bank revenues, with wealth management making up the vast majority. This level of revenue diversification is consistent with the strategy we launched in 2012, and we feel relatively confident that we will meet this target.

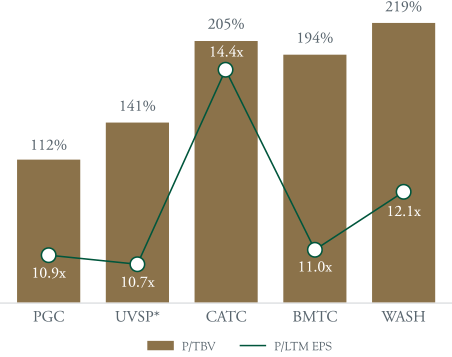

Our Shares Continue to Underperform Compared to Aspirational Wealth Management Peers

The chart below compares our relative valuation to that of our aspirational wealth-based peers. While we have made considerable progress in closing the gap, we continue to believe we are undervalued. We have identified a group of banks with a wealth management focus that carry a premium valuation. As we continue to execute our plan, we believe we will achieve parity providing shareholders with an attractive share price

Note: Pricing data as of December 31, 2018; financial data as reported for the twelve months ended December 31, 2018; Peers are not pro forma for pending or recently closed acquisitions.

*UVSP EPS excludes a charge to the provision for loan and lease losses which represented $0.29 of diluted EPS; including this charge, UVSP P/EPS would be 12.5x.

Peers are UVSP—Univest Financial Corp.; CATC—Cambridge Bancorp; BMTC—Bryn Mawr Bank Corp; WASH—Washington Trust Bancorp.

Source: S&P Global Market Intelligence, company filings

The fact that our shares declined by 28% in 2018, while core earnings per share increased by 17%, illustrates a lack of correlation between our company’s performance and our share price on any given date. We are less concerned with irrational and volatile market behavior and remain singularly focused on executing our strategic plan. We know that over the medium to long term, the highest performing institutions deliver the highest shareholder return.

Wealth Management Had a Tremendous Year Despite the Sell-off in Q4

Wealth management fees increased $10.1 million or 43% in 2018. This growth reflects full year performance of Murphy Capital Management and Quadrant Capital Management, and solid new investment inflows of over $400 million. Additionally, in September, we welcomed Lassus Wherley to the Peapack-Gladstone Bank family. Founded and led by Diahann Lassus and Clare Wherley, this women-owned firm brings with it extensive tax and financial planning expertise. We are currently formalizing plans to expand our financial planning capabilities company-wide. Lassus Wherley contributed four months of revenue to our 2018 total. As we have over the last few years, we will continue to pursue wealth management acquisition opportunities with firms that are culturally similar and that are additive and/or complementary to our company and consistent with our strategic vision.

In 2018, we created a comprehensive plan to integrate and unify our wealth business under a new brand—“Peapack Private.” This comprehensive plan includes streamlining and connecting our investing and research activities, building a common operating and technology framework, and as just mentioned, expanding our financial planning capabilities.

Our Platinum Service Team Grew and Continues to Exceed Client Expectations

In its second full year of operation, deposits managed by our Platinum Service Team grew by 65% or $277 million to $702 million in 2018. This team provides best-in-class banking services to businesses and our most affluent personal clients. The Platinum Service Team also serves as a training platform for our next generation of bankers. During the year, we launched a formal training program and have made plans to hire the next generation of bankers over the next three to five years.

Retail Banking Had Its Best Year Ever

Our Retail Banking team continued to focus on new client acquisitions through our high-touch model and innovative products. During the year, we grew deposits by $197 million. We now have a comprehensive new business strategy for each of our growth markets. This approach places additional manpower and marketing resources in a thoughtful and focused manner. We recently tested this in one of our markets and generated significant new business as a result. To date, client retention has been very strong.

OUTSTANDING

The Inflection from Multifamily to C&I Lending Gained Considerable Momentum

When we launched our strategy—Expanding Our Reach—six years ago, we communicated that we would fund the build-out of our wealth management and commercial lending businesses and make necessary investments in infrastructure, technology, and risk management by expanding our multifamily lending. Multifamily lending in greater New York has historically been a very safe asset class. Knowing that we could grow multifamily quickly and safely, we originated more than $2 billion in loans with no material delinquencies or credit impairment issues.

Multifamily lending provided us the revenue that enabled us to invest in and grow our wealth and commercial businesses. The plan was always to decrease our reliance on this asset class as our business grew. In 2018, C&I loans grew 46% or $440 million while multifamily declined by 18% or $251 million.

Since loan spreads are typically better for commercial loans, we took the opportunity to sell $131 million of longer dated multifamily loans in Q4 2018. The portfolio we sold carried a coupon of 3.28%, which was replaced by shorter-maturity commercial loans with an average coupon of 4.78%. Being opportunistic like this enables us to create shareholder value.

Our commercial real estate business closed $143 million in new loans in 2018. Virtually all of this loan volume was on a floating rate basis, which has helped us navigate rate increases. Clients looking for a fixed rate are accommodated through an interest rate swap arranged through a third party. This activity generated $3.8 million in fee income in 2018—a record.

In addition, our Small Business Administration (SBA) business generated a record of $1.6 million in fee income. SBA fees are generated by selling the government guaranteed portion of an SBA loan. Overall total fees from Swaps, SBA and residential mortgage sales totaled more than $5.8 million in 2018, a 22% increase over 2017.

Sustaining Our Unique Culture is an Important Objective

From my perspective, our company’s culture is what makes us unique and special. As we grow, preserving our culture is a top priority.

In early 2018, we concluded an exhaustive search for a head of Human Resources. Brydget Falk-Drigan joined us from a large international financial service firm. Through her leadership, we now have a well-defined talent development program, we have created a formal onboarding program, established a companywide culture committee, enhanced our internal process for communication, and expanded our recruiting capabilities. Each of these initiatives supports our culture as we continue to grow.

As evidence of our unique culture, in 2018 we were recognized by American Banker as one of the best banks to work for in the United States. We were the only New Jersey bank to receive this prestigious recognition. We believe having employees who love their job and the people they work with drives success. Our culture is what delivers a great experience for our clients who in turn reward us with their trust and ultimately their business. This is our formula for success.

Our Team Continues to Focus on the Client Experience

Over the past two years, Bob Plante, our Chief Operating Officer, along with Kevin Runyon, our Chief Information Officer/Chief Digital Officer, have made significant strides in updating our technology and operations, with an eye toward enhancing the client experience. In 2018, we enhanced our data driven decision making and began focusing on digital, which will enhance the client experience and will help drive cost efficiencies. In addition, we successfully rolled out a comprehensive training platform, an enhanced escrow management system, an automated collateral tracking system, and have embarked on an effort to assess potential vendors for an automated commercial loan system. A thoughtful updated multi-year technology roadmap is being developed, and I expect that we will complete this assessment mid-2019. Technology has become an essential ingredient for our future success.

“In 2018, we were recognized by American Banker as one of the best banks to work for in the United States. We were the only New Jersey bank to receive this prestigious recognition.”

Another Great Year, and We Remain Optimistic About Our Future

We delivered strong results in 2018 and remain optimistic about what is to come. We are taking the necessary steps to thrive in the future. Through our recent growth, we have achieved scale and our unique business model is delivering results. We have a great team, and we are winning our share of business in a very competitive market. Remaining disciplined will continue to deliver future profitability.

There are a number of factors that collectively will drive future increases in share price. First, we operate in three of the top ten most affluent markets in the United States. Second, our key growth businesses— wealth management and commercial banking—are businesses that have considerable scarcity value and barriers to entry, and thus supports a premium valuation. Third, our team has proven that we can drive organic growth and profitability. Fourth, our average deposits per branch now approach $200 million; this provides us with a cost advantage relative to our competition. Fifth, we have a pristine balance sheet with a very strong credit quality. Sixth, we have an enviable capital position. Perhaps most important seventh, we have a tremendously experienced and high-performing team of professionals capable of taking our company to the next level.

In closing, I would like to thank our Chairman, Duff Meyercord, and our Board of Directors for their support and leadership over the past year. A special thanks to John Kissel and Jim Lamb for their service on our Board; both retired effective 01/31/2019. John and Jim have helped guide and strengthen our company, and our entire team is very thankful for their guidance and support.

In February 2019, we welcomed two new Directors to our Board—Peter Horst and Patrick Mullen. Both have unique skills that will help guide us through the next chapter in the execution of our strategic plan.

Peter Horst is a Fortune 500 Chief Marketing Officer with 30 years of marketing leadership across diverse industries in consumer and business products, services and technology for market leaders such as Capital One, General Mills, US West (Century Link), Hershey and Ameritrade. He is the founder of CMO, Inc., and serves as a consultant, author, speaker, board member and advisor to senior executives on marketing strategy, messaging and growth planning.

Patrick Mullen is a highly experienced financial services professional with a distinguished history of team building and effective relationship management. He is an accomplished and seasoned leader, who recently retired as the Director of Banking, State of New Jersey, for the New Jersey Department of Banking and Insurance, for which he worked over the past eight years. There, among other things, he was responsible for the examination and supervision of all state-chartered banks and credit unions and state-licensed non-bank financial institutions.

We welcome Peter and Patrick to the Peapack-Gladstone Bank family.

Once again, many thanks to all of you for your continued support. We appreciate the trust and confidence that you have placed with us.

Douglas L. KennedyPresident & Chief Executive Officer